SINGAPORE, 16 July 2024 (Tuesday) - These are the research findings of the 52nd round of the DBS-SKBI Singapore Index of Inflation Expectations (SInDEx) Survey at the Sim Kee Boon Institute for Financial Economics (SKBI), Singapore Management University (SMU).

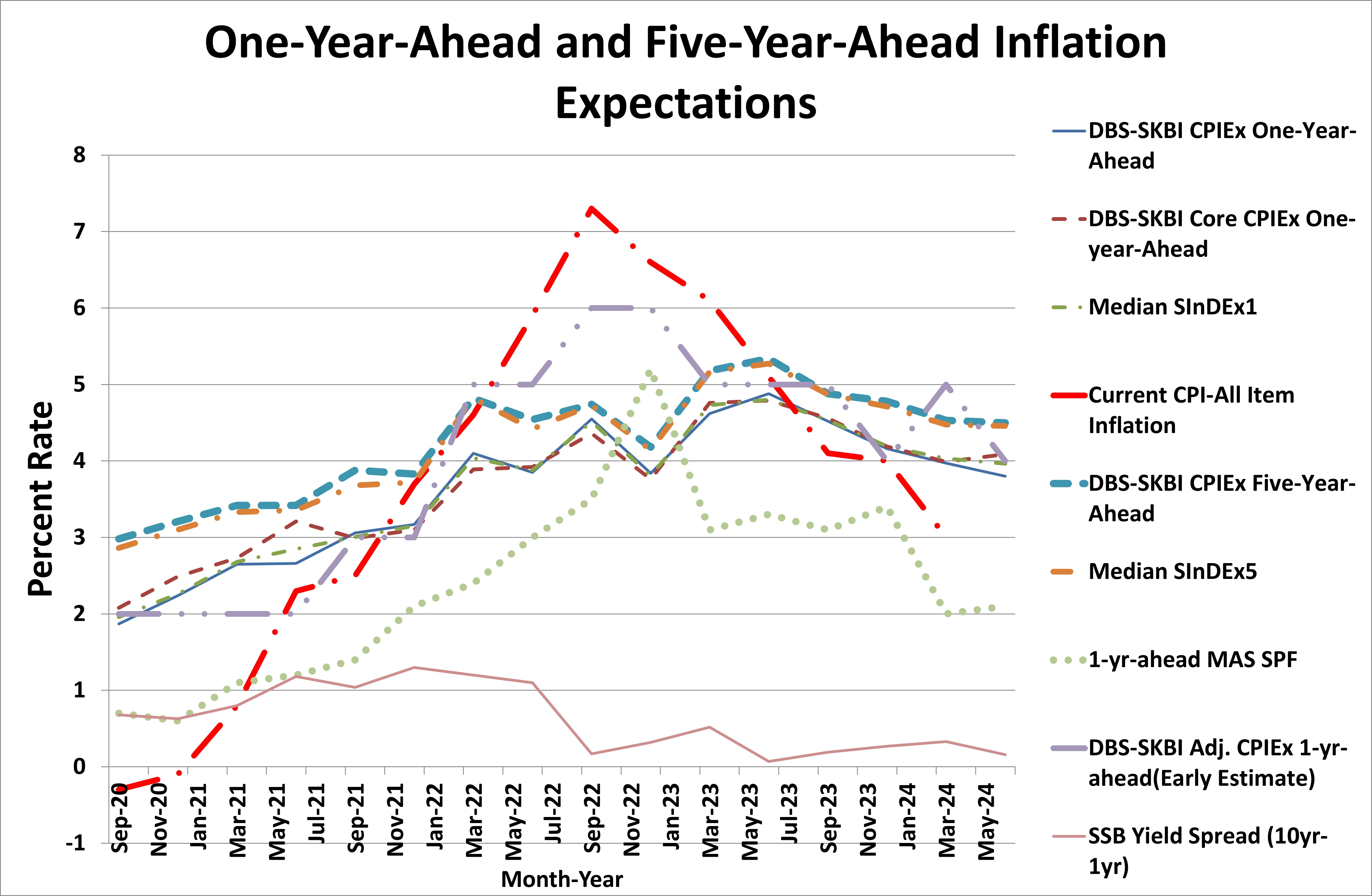

- One-year-Ahead headline inflation expectations pared to 3.8% in June 2024 from 4.0% in March 2024. Consumers’ headline inflation expectations maintained a slow downward trajectory, in line with general global trends in major economies, responding to continued but circumspect restrictive monetary policy. Nonetheless, the second quarter One-year-Ahead inflation expectations continue to be higher than the average One-year-Ahead headline inflation expectations of 3.4% since the inception of this index in the third quarter of 2011.

- As a comparison benchmark, data from the Monetary Authority of Singapore Survey of Professional Forecasters (MAS SPF) released in June 2024 showed that the median forecast of the Consumer Price Index (CPI)-All Items inflation for 2024 was 2.8% (for 2025, 2.1%) while MAS Core Inflation median forecast was 3.0% (for 2025, 2.0%) (MAS SPF June 2024, Table 2 and Table A.5). The latest CPI data release from the Department of Statistics showed that CPI-All Items rose by 3.0% between January and May 2024, compared to the same period in 2023, with the latest May 2024 monthly inflation print coming in at 3.1% year-on-year. On 12 April 2024, in their second quarterly policy review in 2024, MAS maintained the rate of appreciation of the Singapore Dollar Nominal Effective Exchange Rate (S$NEER) policy band, following five consecutive tightening moves between October 2021 and October 2022. The current appreciating path of the S$NEER policy band is intended to continue to reduce imported inflation and help curb domestic cost pressures, thereby ensuring medium-term price stability. The next monetary policy statement will be announced by end July 2024.

- The overall Consumer Price Index Inflation Expectations (CPIEx), after adjusting for potential component-wise behavioural biases and re-combining across components, dropped significantly to 4.2% in June 2024 from 4.9% in March 2024. One-year-Ahead inflation expectations of major components of CPI dropped, namely in components like Food (from 5% to 4%), Transportation (from 5% to 4.5%), Housing & Utilities (from 5% to 4%), Education (from 5% to 4%), Recreation & Culture (from 5% to 4%) and Miscellaneous Goods & Services including Personal Care (from 5% to 4%), while other components like Healthcare (at 5%), Household Durables & Services (at 4%), Clothing & Footwear (at 4%), Communications (at 4%) stayed unchanged in June 2024 compared to the March 2024 polling. This broad-based decline in component-based inflation expectations signals that restrictive monetary policy environment are in place, in conjunction with an uneven global growth outlook, as reflected in perceptions of inflation expectations.

- The survey team also polled free-response overall inflation expectations after accommodating potential behavioural biases by informing respondents of current aggregated economic data. We found that the One-year-Ahead headline inflation expectations declined from 5% in March 2024 to 4% in June 2024. After stripping out Accommodation and Private Transportation, the Singapore Core Inflation Expectations also declined from 5% in March 2024 to 4% in June 2024. These free-response polls help us to gauge perceptions of anchoring of inflation expectations and consumer sentiments in an aggregated sense.

- Overall, responding to global cues of geo-political tensions in a largely bifurcated global order, fallout from ongoing conflicts between Hamas and Israel and Ukraine and Russia, and ‘higher for longer’ global interest rates in place to tackle petulant inflationary pressures particularly by the US Federal Reserve Board, Singaporean consumers expect a slight negative impact on the country’s economic growth over the next 12 months.

- In addition, despite a more broad-based decline in inflation expectations and general cost-of-living pressures, Singaporean consumers also opined that over the next 12 months, their overall expenses are expected to increase slightly.

- In the June 2024 survey, Singaporean consumers polled were almost equally split on how they felt the overall One-year-Ahead inflation scenario would unfold in the next 12 months. Around 45.2% (compared to 45.9% in March 2024) of those surveyed expect inflation to decline in the medium term of one year while 45.4% (compared to 45.9% in March 2024) felt that One-year-Ahead inflation will increase. This result shows the cognitive dissonance and disagreements coming from the high level of uncertainty that is plaguing the global economy, policy environment and fallout of ongoing conflicts in the medium term of one year.

- The main reason cited by those expecting inflation to decline is the role of central banks in keeping interest rates high (36%). The slowdown of global growth was cited as the second most common reason by respondents (32%). A distant third, given by 22% of respondents, was that the resolution of supply chain disruptions is also expected to relieve price pressures. Among respondents expecting inflation to increase over the next 12 months, there was more diversity in opinion. The most common reason cited was the impact of higher interest rates by the central banks of major economies (29%). This was followed by geopolitical uncertainties due to the conflicts between Hamas and Israel, and Ukraine and Russia (24%), and high demand due to the easing of pandemic-era measures (16%). Fiscal measures such as the hike in GST (14%) and supply chain disruptions (13.5%) were cited as other possible major reasons.

-

In the June 2024 survey, respondents opined that current economic conditions have a limited negative impact on One-year-Ahead but no discernable impact on the Five-year-Ahead overall inflation expectations. Component-wise, respondents expect no discernable impact on inflation related to Food, Transportation, Housing & Utilities, Healthcare, Education, Household Durables & Services, Recreation & Culture, Communications, Clothing & Footwear, and Miscellaneous Goods & Services. We observe a significant variation of perspectives possibly due to lived experience or behavioural bias among the respondents, which results in bimodal distributions with one segment of the population expecting a decline in inflation while another expecting an increase in inflation, both in overall and component-wise measures.

- Alberto Cavallo of Harvard Business School (Cavallo, 2020) and a report by the European Central Bank (Kouvavas et al., 2020) highlighted potential biases in CPI calculations with fixed baskets as respondents made substantive changes to their consumption baskets owing mainly to the COVID-19 pandemic. In the June 2024 survey, Singaporean consumers polled that in the next 12 months they expect no change in budget share of expenses for Education, Recreation & Culture, Communications, Clothing & Footwear, and Miscellaneous Goods & Services. However, the respondents expect a slight increase in the budget share of expenses in Food, Transportation, Housing & Utilities, Healthcare and Household Durables & Services. These results indicate that respondents expect their consumption baskets to change over the next 12 months. This means some respondents expect a higher proportion of budget or higher budget share on certain components over the next 12 months, compared to other components. These changes in budget share can potentially be due to more permanent changes in consumption behaviour in the post-pandemic era, like the practice of working from home regularly or ordering groceries online rather than buying them in-store. Furthermore, unlike the impact perception of components of inflation, there is no discernable bimodality or disagreement in the responses on changes of budget share. The changes in the budget share are substantive and signal more permanent changes in consumption patterns across the board.

- Excluding inflation expectations in Accommodation and Private Transportation, the One-year-Ahead CPIEx core inflation expectations for this SInDEx survey inched up to 4.1% in June 2024 compared to 4.0% in March 2024. This is slightly surprising and signals that the decline in overall inflation was probably due to higher declines in more volatile components in Accommodation or Private Transportation, rather than equivalent declines in all components of CPI.

-

For a subgroup of the population who owns their accommodation and uses public transport, the One-year-Ahead CPIEx core inflation expectations inched up to 4.1% in June 2024 from 3.9% in March 2024 – verifying the robustness of the findings in the slightly surprising increase in core inflation expectations. This sub-sample measurement is potentially more representative and hence more accurate than the full sample measurement, due to high home ownership and public transport ridership in Singapore.

-

Unlike the fixed radio-button response which might be susceptible to various behavioural biases, core CPIEx Inflation Expectations (excluding Accommodation and Private Transportation expenses), after adjusting for potential component-wise behavioural biases and re-combining across components, pared down to 4.1% in June 2024 from 4.8% in the March 2024 survey. The free-response core CPIEx, also declined to 4% in June 2024 from 5% in March 2024. The convergence among these cognitive measures of perception of inflation expectations gives us some assurance that even after addressing some changes in price levels, individual households often adapt to current conditions and update their baskets accordingly, and come out with similar expectations. Having said that, fixed basket calculations like CPI can give us potentially higher inflation figures, a more representative and less volatile measure might be the core per capita consumption expenditure (core PCE) typically used by central banks like the Federal Reserve Board.

-

The One-year-Ahead composite index SInDEx1 that puts less weight on more volatile components like Accommodation, Private Road Transport, Food and Energy-related expenses remained unchanged at 4.0% in June 2024 compared to the March 2024 survey. It continued to be higher than the second quarter average of 3.5% during the survey’s existence from 2011 to 2023.

-

In addition, in June 2024, 8.9% Singaporeans polled expect a more than 5.0% reduction in salary in the next 12 months, slightly higher than 7.8% in the March 2024 survey, so no significant decline in the job outlook was detected. The expectations of median salary increments of between 1.0% to 5.0% also remained unchanged, compared to the March 2024 survey.

DBS Bank Chief Economist and Managing Director of Group Research, Dr Taimur Baig commented, “A combination of tight monetary policy and favourable supply side conditions have brought down headline and core inflation appreciably over the past year, and expectations have begun to adjust accordingly. We welcome these favourable developments, as they help mitigate the cost-of-living difficulties faced by the population in recent years.”

Dr Aurobindo Ghosh, Assistant Professor of Finance at Singapore Management University (SMU), the creator and the founding Principal Investigator of the Quarterly DBS-SKBI SInDEx Project, observed, “The Survey of Consumer Expectations (SCE), an online representative monthly survey conducted by the New York Federal Reserve, in their most recent press release revealed a decline in one year and five year ahead inflation expectations by about 0.2%, and a general decline in specific goods prices in the United States. There is also a general decline in uncertainty or disagreement. The quarterly SInDEx survey more or less reflects the findings among Singapore households, except there seems to be an uptick in the One-year-Ahead Singapore or MAS core inflation which excludes Accommodation and Private Transportation. There are two quick observations. First, the Singapore or MAS core inflation excludes policy-driven accommodation and private transportation components, unlike the international core inflation that excludes more volatile fuel and food prices. So a closer look reveals that expectations of Accommodation and Private Transportation costs might have gone down faster than the other components. Second, the strong Singapore dollar has dampened imported inflation of higher US dollar denominated prices but some passthrough impacts might still be present. However, the overall price impact is the net effect of the perceptions on several components described above. In sum, medium term or One-year-Ahead headline inflation expectations have inched down, similar to the findings of the NY Federal Reserve’s Survey of Consumer Expectations. Even after addressing behavioural biases in respondents, this decline seems broad-based across different components (Clark, Ghosh and Hanes, 2018), though the decline seems uneven across headline and core inflation expectations.”

“One aspect of Consumer Price Index (CPI) based inflation reflects the comparison of prices of a fixed basket of goods and services identified to be a representative basket by the five-yearly Household Expenditure Survey (HES) last conducted pre-pandemic (HES 2017/18), which might have changed permanently, as work from home arrangements have become more standard (Cavallo, 2020, Kouvavas et. al.,2020, Weber et. al., 2022). There is an even split between respondents who feel inflation will go down (about 45.2%) and those who feel prices will go up (about 45.4%), both groups feel a major reason is the policy action of central banks keeping an international interest rate ‘higher for longer.’ This level of cognitive dissonance is also holding policymakers like US Federal Reserve Chair Jerome Powell back from starting to normalise rates prematurely, and waiting for more data, to avoid a resurgence of debilitating inflation. Hence, it is not surprising that the Monetary Authority of Singapore has kept their tight policy stance unchanged in their April 2024 Monetary Policy Review, while they closely monitor global and domestic economic developments as stated in MAS Monetary Policy Statement of April 2024.”

For the longer horizon, the Five-year-Ahead CPIEx inflation expectations remained unchanged in June 2024 at 4.5% compared to March 2024. The current polled number continues to be slightly higher than the second quarter average of 4.2% polled since the survey’s inception in September 2011 up till 2023.

The Five-year-Ahead CPIEx core inflation expectations (excluding costs related to Accommodation and Private Road Transportation) also remained unchanged at 4.5% in June 2024 compared to March 2024. Overall, the composite Five-year-Ahead SInDEx5 also remained unchanged at 4.5% in June 2024 compared to March 2024. In comparison, the first quarter average value of the composite Five-year-Ahead SInDEx5 is 4.1%, since the survey’s inception in September 2011 till 2023.

After adjusting for potential behavioural biases, the free-response Five-year-Ahead Headline Inflation Expectations remained unchanged at 5% in June 2024 from March 2024, while the free-response Core Five-year-Ahead Inflation Expectations also remained unchanged in June 2024 at 5% compared to March 2024. We observe that long-term inflation expectations, both headline and core, remained constant despite global uncertainty, signaling the anchoring of long-term inflation expectations.

Dr Aurobindo Ghosh added, “DBS-SKBI SInDEx survey respondents polled long-term inflation expectations both for the Five-year-Ahead Headline as well as the Core Inflation Expectations continuing stayed pat in June 2024 survey. Even after adjusting for behavioural biases, the long-term inflation expectations remained flat after declining over the last four quarters. This corroborates with the findings of the importance and accuracy of survey based measures (Ang, Baekert and Wei, 2007), and also reflects informed opinion among Singaporean consumers who opined that uncertainty in the short term will reduce in the longer term, Overall, despite short-term unevenness in inflationary expectations there is anchoring of long-term inflation expectations, perhaps inching to a new normal."

Methodology

DBS-SKBI SInDEx survey yields CPIEx Inflation Expectations (estimating headline inflation expectations) and related indices are products of the online quarterly survey of around 500 randomly selected individuals representing a cross section of Singaporean households. The survey is led by Principal Investigator Dr Aurobindo Ghosh, Assistant Professor of Finance (Education) at Lee Kong Chian School of Business of the Singapore management University. The online survey, powered by Agility Research and Strategy, helps researchers understand the behavior and sentiments of decision makers in Singaporean households. DBS Group Research is a co-sponsor and research partner with the Sim Kee Boon Institute for Financial Economics (SKBI) at SMU.

The quarterly DBS-SKBI SInDEx survey has also yielded two composite indices, SInDEx1 and SInDEx5. SInDEx1 and SInDEx5 measure the One-year inflation expectations and the Five-year inflation expectations, respectively. The sampling was done using a quota sample over gender, age and residency status to ensure representativeness of the sample. Employees in some sectors like journalism and marketing were excluded as that might have an effect on their responses to questions on consumption behavior and expectations.

The DBS-SKBI SInDEx survey was augmented in June 2018, based on a joint research study conducted by SMU researchers in collaboration with MAS and the Behavioural Insights Team, where respondents were polled on their perceptions of components of the Consumers Price Index (CPI) and adjusted for possible behavioural biases prevalent in online surveys.

Based on the recommendations of the joint study, since March 2019 the research team has polled the One-year-Ahead inflation expectations of all of the major components of CPI-All Items inflation. For June 2024 survey, DBS-SKBI CPIEx headline inflation expectations indices declined compared to March 2024. The core inflation expectations however inched up. The behaviourally adjusted component-wise and recombined inflation expectations declined almost across the board, except for Clothing & Footwear, Household Durables & Services and Communications inflation expectations remained unchanged. In free-response answers, compared to March 2024 survey, responses in the June 2024 survey polled for One-year-Ahead Headline and Core Inflation Expectations declined. Overall, the results indicate continued slowdown in the medium term and flattening of long inflation expectations.

We introduced a new ratio in the June 2020 survey, on the life versus livelihood debate as an aftermath of the Covid-19 pandemic – the ratio of respondents who feels livelihood should be prioritised over life vis-à-vis those who feel the other way. This ratio declined to about 2.7 in June 2024 from 4.7 in March 2024. For every respondent who prioritised life over livelihood, there were about 3 who prioritised livelihood over life, signalling life returning to normal with an endemic Covid-19 in Singapore and focused on economic growth.

References:

Ang, A., G. Bekaert, and M. Wei., 2007, “Do Macro Variables, Asset Markets, or Surveys Forecast Inflation Better?” Journal of Monetary Economics, 54:4, pp. 1163–212.

Cavallo, A., 2020, "Inflation with COVID Consumption Baskets." NBER Working Paper Series, No. 27352, June 2020 (Harvard Business School Working Paper, No. 20-124, May 2020). (https://www.hbs.edu/faculty/Pages/item.aspx?num=58253, accessed on July 14, 2020)

Clark, A., A. Ghosh and S. Hanes, 2018, “Inflation Expectations In Singapore:

A Behavioural Approach,” Macroeconomic Review, Vol 17:1, pp. 89-98.

Household Expenditure Survey (HES 2017/18): (https://www.singstat.gov.sg/publications/households/household-expenditu…, accessed on July 10, 2024)

Kouvavas, O., R. Trezzi, M. Eiglsperger, B. Goldhammer and E. Goncalves, 2020, “Consumption patterns and inflation measurement issues during the COVID-19 pandemic,” ECB Economic Bulletin, Issue 7/2020. (https://www.ecb.europa.eu/pub/economic-bulletin/html/eb202007.en.html#t…, accessed on July 14, 2020)

MAS Monetary Policy Statement - April 2024, (https://www.mas.gov.sg/news/monetary-policy-statements/2024/mas-monetar…, accessed on April 12, 2024)

MAS Survey of Professional Forecasters (MAS SPF), June 2024, (https://www.mas.gov.sg/-/media/mas-media-library/monetary-policy/mas-su…, accessed on July 9, 2024)

Singapore Consumer Price Index Press Release, June 2024, Singapore Department of Statistics (https://www.singstat.gov.sg/-/media/files/news/cpimay24.ashx, accessed on July 9, 2024)

Survey of Consumer Expenditure (SCE), 2024, “Consumers Expect Lower Inflation and Slower Home Price Growth Over the Next Year,” (Press Release on July 8, 2024), (https://www.newyorkfed.org/newsevents/news/research/2024/20240708, accessed on July 10, 2024).

Weber, M., F. D’Acunto, Y. Gorodnichenko and O. Coibion, 2022, “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications,” Journal of Economic Perspectives, 36:3, pp. 157–184.

END